Low Credit Score? This One Number Can Kill Your Home Loan Dreams

Many Indians have one dream in common and they have a thing for this dream and that is owning a house. A lot of Indians spend lakhs of rupees or even crores of rupees to fulfill this dream.

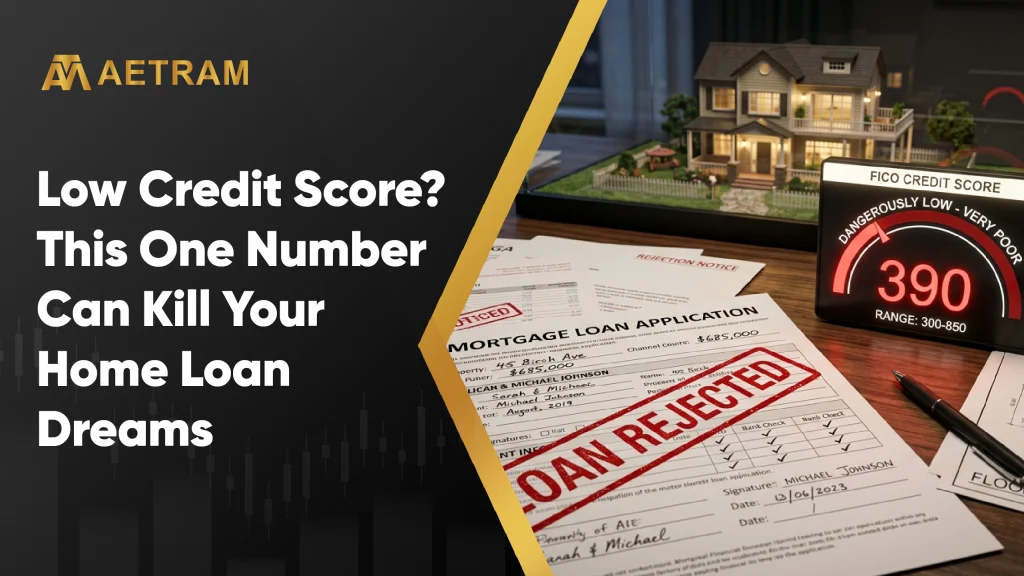

They would have spent loads of time to finally find the right property at a price that fits their budget. So they decide to walk into the bank to apply for a home/housing loan with an application form in hand and full of hope. But after the initial process and vetting, the loan officer delivers the unfortunate verdict and that is your housing loan application has been rejected.

There is no fraud by the applicant or missing documents or income problems for the applicant and it is just a score called CIBIL credit score. This is not a hypothetical situation but a reality for millions of Indians.

A low credit score can quietly destroy your home loan dreams even before you get a chance to think of building your house. The cruel irony is that most people do not know what their credit score is until the moment it costs them the most. This is the one number that is more important when you think of owning a house and it has more power over your homeownership journey compared to your salary, your savings or even your reputation.

In this blog, we will discuss what a credit score is and how it decides your fate of owning a house and what you can still do about it.

What is a CIBIL credit score?

In India, a credit score is given by TransUnion CIBIL which is India’s most widely trusted credit bureau. A CIBIL credit score is a three-digit number ranging from 300 to 900 and it is a numerical summary of your entire credit life. It tells the lender about every loan you have taken, every EMI you have paid or missed and every credit card bill you have cleared or skipped or postponed.

Why does it hold so much power?

The credit score given by CIBIL carries so much weight with lenders because a home loan is not a small commitment and it is typically a 15 to 30-year relationship involving crores of rupees. The lender needs a solid reason to trust you before they make a huge commitment. And the trust in the world of lending is measured in three digits.

According to data from TransUnion CIBIL, approximately 79% of loans are approved for borrowers with scores above 750. With most lenders in India using CIBIL credit score as the primary filter, your score is not just a number but it is about your financial prudence and your credit history.

How a low score quietly makes your home more expensive

You may be happy getting a home loan even with a low credit score but the real caveat would be the lender would have sanctioned the loan with a higher interest rate. Banks follow what is known as risk-based pricing which is nothing but if a lender thinks a potential borrower is risky based on their evaluation, then they will charge higher interest rate for that borrower.

Consider there are two borrowers who want a Rs 50 lakh home loan for a period of 20 years. Borrower 1 has a credit score of 810 and Borrower 2 has a credit score of just 730. Borrower 1 will be offered a housing loan at a lower interest rate (for example 8.5%) compared to Borrower 2 who would be offered a home loan at a higher interest rate, say 9.5% or more, but definitely not at 8.5%.

This one percentage point difference translates to several lakhs in additional interest paid over the life of the loan. Even a 0.5% difference on a ₹1 crore loan over 20 years can cost you upwards of ₹8 lakh extra. Your CIBIL score, in very real terms, determines how much your home ultimately costs you.

Hidden reasons for a low credit score

A lot of people think that they have a good credit score because they assume that they have taken loans and closed it successfully. But there are common and many overlooked reasons that may impact your credit score.

Your credit score can be impacted negatively even if you miss one EMI payment. Your payment history accounts for one-third of your credit score and it is the single largest factor. A single missed EMI can weigh on your credit score significantly and the record stays on your report for years.

Then there is high usage of your limit on your credit cards. Your credit utilisation ratio which is how much of your available credit limit you are actively using contributes another 30% to your credit score. Consistently using more than 30 to 40% of your credit card limit signals financial stress to lenders.

Applying for too many loans at once is also a negative sign. Every time a lender checks your credit profile in response to a loan application, it registers as a “hard inquiry.” A lot of these inquiries within a short period of time will indicate that you are heavily dependent on credit to achieve your goals and may affect your credit score.

Some borrowers would find it difficult to pay the interest and the principal amount and they would go for settlement instead of closing the loan account. In that case you would have paid less than the full outstanding amount to close a loan, your credit report will show the account as “Settled” and not as “Closed.” This is a red flag for lenders and this would not disappear easily from your credit history report.

Your credit score may reduce due to errors in your credit report. This is more common than most people realise. For example, a loan account which was closed by the borrower but not marked as closed by the lender and still showing active due to a clerical mistake can adversely impact your credit score.

No credit history problem

Many first time home loan borrowers may not have a credit history. They would have not taken any kind of loans earlier and they would have dealt most of their payments in cash. So their credit score would show up as “NH” (No History) or “-1.”

This means there is simply no credit data to evaluate. As a result, banks and many lenders find this almost as uncomfortable as a low score. Without a credit trail, there is nothing to judge a borrower’s repayment behaviour.

If this is your situation, your application may be dependent solely on your income documents like consistent salary slips, three years of income tax returns and bank statements that show healthy inflows, regular savings and no bounced cheques. Your occupational stability becomes the substitute for credit history. You may also apply for a credit card with a lower limit and use the card judiciously to start building your credit history.

Low credit score is not end of your dream

A low CIBIL credit score can be a setback for home loan borrowers but there are ways to make your dream home come true.

You can approach NBFCs and Housing Finance Companies (HFCs) in case scheduled commercial banks reject your loan application. Traditional banks operate under strict RBI rules and they mandatorily follow the regulations laid down by the central bank. But NBFCs and HFCs have more flexibility in terms of internal risk assessment policies. They often look at your income, employment history, existing obligations, value of the property, etc. rather than filtering solely on the score. The trade-off is higher interest rates compared to banks.

You may also add a co-applicant with a strong credit profile. If your spouse or a close family member has a CIBIL score above 750 and a stable income, adding them as a co-applicant on the loan can significantly change the lender’s risk calculation. Their creditworthiness will add weight to your loan application and the combined income boosts your eligible loan amount.

A financial guarantor with a good credit profile and history can add an assurance and help the lender process your home loan approvals. The guarantor need not co-own the property but must agree to take the responsibility of repayment if you default.

If you are willing to increase your down payment, then the chances of your home loan application getting accepted increases. Lenders typically finance 75% to 90% of the property’s value but if you manage to pay 30% to 40% upfront instead of the standard 10% to 20%, you reduce the lender’s exposure considerably. A smaller loan request from a riskier borrower is far more agreeable for the lender than a large home loan.

Conclusion

Your credit score is not just a financial indicator but one of the important numbers that will decide your eligibility for a home loan. It is the gatekeeper for one of the most important decisions of your life and a good score will lead to quicker approvals, cheaper interest rate and better negotiation with the lender. In contrast, a poor credit score will lead to higher interest rates, higher processing fees, etc. and cost you a lot of money.

But there is a silver lining because with good financial behaviour, a clear knowledge of what motivates the number and the correct approach for your present circumstances, the path to owning your home is wide open.

So, look at your credit score today and know exactly where you are and start taking the steps to improve your credit score before knocking on the doors of banks.

Frequently Asked Questions (FAQs)

1. What is a good credit score for a home loan?

A score of 750 and above is considered a good credit score for a borrower. Most lenders approve loans faster, offer lower interest rates and require minimal documentation for borrowers in this range.

2. Can I get a home loan if my credit score is low?

Yes. You can negotiate and explain your position to the bank manager and you may get a home loan albeit at a higher interest rate. If a bank rejects your loan application, approach NBFCs or HFCs or add a co-applicant with a strong score or increase your down payment or bring in a guarantor. These measures may improve your approval chances.

3. How can I improve my credit score?

Automate EMI payments, do not keep any dues or postpone your loan repayment, keep credit card usage under your limit, avoid multiple loan applications, retain old accounts and dispute any errors on your CIBIL report immediately.

4. What are the reasons for home loan rejection?

Low credit score, missed EMI payments, high credit utilisation, multiple hard inquiries, settled loans showing on your report and errors in your credit report are the common reasons for rejection.

5. What do banks check besides credit score for a home loan?

Banks evaluate your income stability, employment history, property value, existing loan obligations, bank statements, income tax returns to assess your overall repayment capacity beyond just the credit score.